.webp)

Financial reports are published. The numbers are all there. Revenue, costs, margins, cash flow.

But for most readers, one question still remains. What actually caused these numbers to change? This is where Management’s Discussion and Analysis (MD&A) becomes essential.

Financial statements show outcomes. They do not explain decisions, conditions, or risks. MD&A exists to bridge that gap.

It is the section where management explains what happened, why it happened, and what may happen next.

This article breaks down what MD&A actually involves, what it covers, why it matters, and how it should be interpreted.

What is Management Discussion and Analysis (MD&A)

Management Discussion and Analysis (MD&A) is a required section in a company’s annual report or SEC filings like Form 10-K or Form 10-Q.

It is written by the company management.

It explains three things:

- - How the company performed during the period

- - What its current financial position looks like

- - What risks, trends, or uncertainties may affect future performance

MD&A is not a repetition of financial statements.

It is an explanation layer that connects:

- - Numbers

- - Business activity

- - External conditions

Unlike the balance sheet or income statement, it does not focus on figures alone. It focuses on interpretation.

It allows investors to understand the business through management’s perspective.

What an MD&A Section Actually Does

An MD&A section is not just commentary. It serves a structured role in financial reporting.

It helps investors answer specific questions:

- - What caused revenue or cost changes?

- - Are these changes recurring or temporary?

- - What conditions are affecting the business?

- - Are current results likely to continue?

This is why it is required in regulatory filings.

The goal is not storytelling. The goal is to reduce the gap between reported numbers and real business activity.

Why MD&A Exists in Financial Reporting (H2)

Before MD&A requirements, financial reports had a limitation.

They showed:

- - What happened

- - How much changed

But they did not explain:

- - Why it happened

- - Whether it would happen again

MD&A addresses this gap by requiring companies to:

- - Explain material changes

- - Disclose known risks and uncertainties

- - Describe trends that could affect future results

In practical terms, MD&A is designed to help investors judge:

- - The quality of earnings

- - The sustainability of performance

- - The direction of the business

What Does MD&A Typically Cover (Core Components)

While formats vary, most MD&A sections follow a consistent structure.

1. Results of Operations

This section explains how the company performed during the reporting period.

It focuses on changes in:

- - Revenue

- - Cost of goods sold

- - Operating expenses

- - Profit margins

The key point is not the numbers themselves. It is the explanation behind them.

For example:

- - Revenue increased due to higher sales volume or pricing changes

- - Costs increased due to inflation or supply constraints

- - Margins declined due to higher input costs

This section often includes comparisons with previous periods, such as year-over-year changes.

2. Liquidity and Capital Resources

Liquidity refers to the company’s ability to meet short-term obligations. Capital resources relate to long-term financial strength.

This section explains how the company manages its financial position.

It focuses on:

- - Cash flow analysis

- - Working capital position

- - Debt levels

- - Funding sources

It also covers:

- - Capital expenditure plans

- - Financing strategy

- - Ability to meet short-term and long-term obligations

Investors use this section to assess whether the company can operate without financial stress and support future growth.

3. Known Trends and Uncertainties (H3)

This is one of the most critical parts of MD&A.

Companies are required to disclose events or conditions that are reasonably likely to affect future performance.

These are not general risks. They are identifiable factors such as:

- - Inflation and rising costs

- - Changes in consumer demand

- - Supply chain disruptions

- - Regulatory or political changes

The purpose is not prediction. It is transparency.

If management is aware of a factor that could impact performance, it must be disclosed.

4. Critical Accounting Estimates

Some financial figures are based on judgment rather than the exact measurement. This section explains those areas.

Common examples include:

- - Asset valuation

- -Inventory accounting methods

- - Bad debt provisions

- - Tax estimates

These estimates can significantly influence reported results.

By explaining them, companies allow investors to understand how sensitive financial outcomes are to changes in assumptions.

5. Off-Balance Sheet Arrangements

Not all financial obligations appear directly in the balance sheet.

Some are disclosed separately because they still carry risks.

Examples include:

- - Lease agreements

- - Guarantees

- - Contingent liabilities

MD&A provides visibility into these arrangements so investors can assess total financial exposure.

Purposes of MD&A (Why It Matters)

The purpose of MD&A is not to repeat financial data. It is to make that data understandable.

It focuses on explaining what the numbers represent and how they relate to actual business performance.

It helps to:

- - Break down the reasons behind changes in revenue, costs, and profit

- - Show whether earnings are driven by core operations or temporary factors

- - Present management’s interpretation of performance and strategy

- - Connect financial results with operational and market conditions

- - Highlight risks and trends that may affect future performance

- - Provide insight into whether current results are likely to continue

MD&A and Regulatory Requirements

According to U.S. SEC rules, MD&A is required for public companies.

In the United States, it must be included in:

- Form 10-K (annual filing) - appears under Item 7

Although MD&A is not audited like financial statements, companies are required to present information that is:

- - factual

- - balanced

- - not misleading

What Makes an MD&A Useful

Not all MD&A sections provide the same level of insight.

A useful MD&A typically:

- - Clearly explains the causes behind financial changes

- - Uses specific data instead of vague language

- - Compares current performance with prior periods

- - Focuses on material issues that affect decision-making

- - Presents both positive and negative developments

When these elements are missing, the section becomes less informative.

How Investors Actually Use MD&A

Investors do not rely on MD&A alone. They use it alongside financial statements to understand what the numbers actually mean in practice.

In most cases, the section is used to answer specific questions that financial data cannot explain on its own.

1. To Validate Financial Trends

Investors compare MD&A explanations with reported results.

If revenue or profit changes, they look for:

- - what specifically caused the movement

- - whether the explanation aligns with the numbers

If the explanation does not match the data, it raises concerns about reliability.

2. To Identify Risks Early

Some risks are not visible in financial statements.

MD&A highlights factors such as:

- - cost pressures

- - demand changes

- - operational challenges

This helps investors understand potential issues before they affect reported performance.

3. To Assess Earnings Sustainability

Not all earnings are repeatable.

Investors use MD&A to determine whether results are:

- - driven by core operations

- - influenced by temporary or one-off factors

This is critical when evaluating long-term value.

4. To Understand Management Priorities

MD&A shows what management is focusing on.

This includes:

- - growth areas

- - cost control efforts

- - investment decisions

It provides insight into how the business is being managed going forward.

5. To Evaluate Future Outlook

Investors use MD&A to interpret forward-looking information.

They assess:

- - expected trends

- - potential risks

- - overall direction of the business

This helps shape expectations about future performance.

6. To Check Consistency Across Reporting

Investors compare MD&A with:

- - financial statements

- - prior disclosures

- - external market conditions

Any inconsistency may signal gaps in reporting or overly optimistic interpretation.

Real-World Example of Management Discussion and Analysis

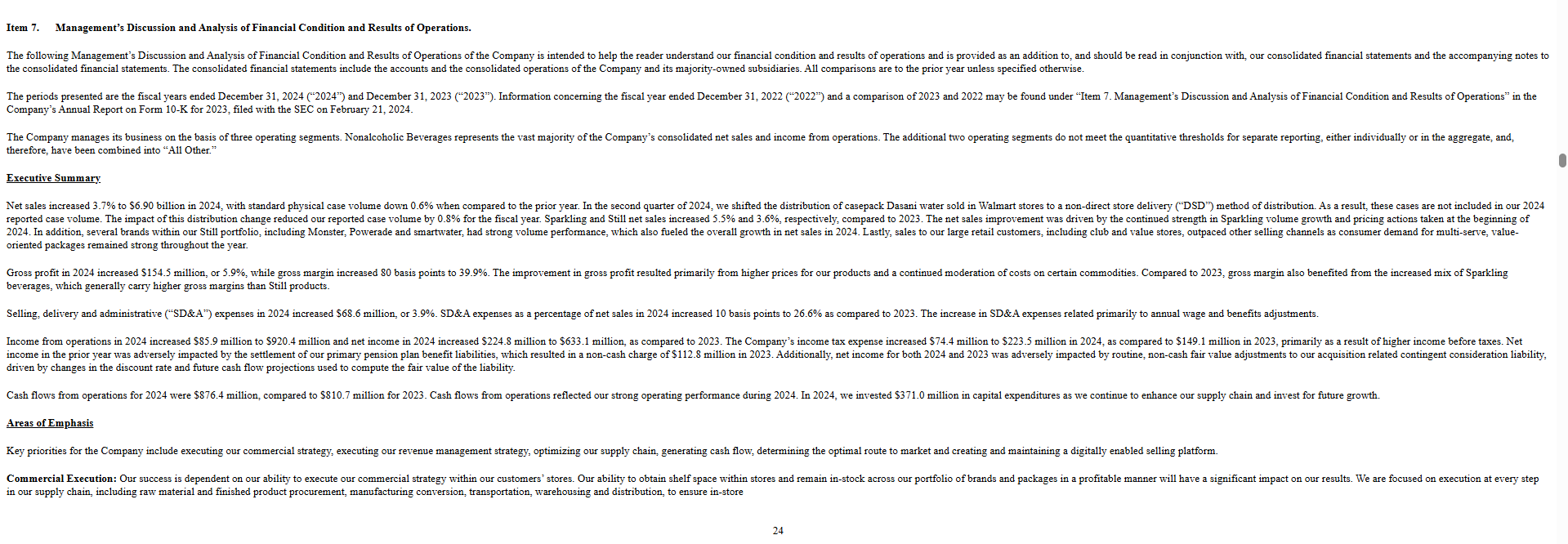

You can review a real example in Coca-Cola’s 2024 Form 10-K, where management explains revenue drivers, cost changes, and business conditions in its MD&A section.

Where MD&A Can Fall Short

Despite its usefulness, MD&A has some limitations:

1. Not Audited

Unlike financial statements, MD&A is generally not audited by independent accountants.

2. Subject to Bias

Since it is written by management, it may present a more favorable view of the company.

3. Limited Disclosure of Strategy

Companies may avoid revealing sensitive business strategies to protect their competitive advantage.

4. Forward-Looking Uncertainty

Future projections may not always be accurate.

For these reasons, MD&A should always be read alongside financial statements.

Bottom Line

Management’s Discussion and Analysis is a core part of financial reporting. It connects numbers with business reality.

When done properly, it helps investors understand performance, risks, and future direction. When it is unclear or incomplete, it limits the usefulness of the entire report.

For anyone analyzing a company, MD&A is not optional reading. It is where the explanation happens.

Quantillium offers an all in one corporate filings API across global markets. Use our standardized API to speed up research and analysis. Explore the API Docs or Start a free trial to get started.

Frequently Asked Questions

Where is the MD&A section found?

The MD&A section is included in company SEC filings such as Form 10-K (annual filing) and Form 10-Q (quarterly filing). In a 10-K, it typically appears under Item 7.

Who prepares the MD&A section?

The MD&A is written by company management, usually senior executives like the CEO, CFO, or finance leadership team.

Is MD&A audited?

No. It is not audited in the same way as financial statements. However, companies must ensure that the information is accurate, balanced, and not misleading.

What does MD&A include?

MD&A typically includes analysis of operations, liquidity, capital resources, risks, accounting estimates, and future outlook.

How is MD&A different from financial statements?

Financial statements present numerical data, while MD&A explains those numbers by providing context, analysis, and management’s perspective.

Do private companies need MD&A?

Private companies are generally not required to include MD&A, but some may provide similar analysis to improve transparency for stakeholders.

Does MD&A include future predictions?

Yes. MD&A often discusses trends, risks, and conditions that may affect future performance, helping investors assess what may happen next.

.webp)

.webp)

.webp)